Iran Conflict 2026: Asia‑Pacific Faces Sustained Macro Shock from Gulf Supply Disruption

Context

Disruption to Gulf energy, fertiliser, and chemical feedstock production and transit represents a structurally significant risk to Asia Pacific economic stability, given the concentration of supply, the region’s high import dependence, and the centrality of maritime chokepoints to these flows.

Saudi Arabia, the United Arab Emirates, Qatar, Kuwait, Bahrain, and Iraq collectively produced 24.7 million barrels of oil per day in 2024, equivalent to 24% of global output, according to US Energy Information Administration (EIA) data.

The same six Gulf states account for 9.5% of global gas production, with Qatar alone contributing 4%. Typically, around one fifth of global liquefied natural gas transits the Strait of Hormuz.

They also supply approximately 15% of global nitrogen fertiliser and remain a critical source of chemical feedstocks, including an estimated 40–50% of global naphtha supply, 23% of ethylene polymer exports, and 19% of sulphur, based on UN COMTRADE data for 2024.

Maritime disruption has substantially constrained these flows. Attacks against shipping have increased transit risk and insurance costs, contributing to a sharp contraction in traffic through the Strait of Hormuz. According to IMF PortWatch data, disclosed traffic volumes were down 92% year on year as of 5 April 2026.

Asia-Pacific exposure to Gulf output is high by global standards. Regional markets accounted for 77% of Qatar’s LNG exports in 2023 and 2024 and 43% of refined petroleum exports, according to UN COMTRADE data.

Asia-Pacific countries also absorb around 15% of Gulf chemical feedstock output. This reliance reflects the region’s manufacturing- and export-oriented economic structures, a structural mismatch between domestic resource endowments and demand, and geographic factors that have historically supported Gulf–Asia supply chains.

A two-week ceasefire in the Iran conflict was announced on 8 April 2026. Implementation was initially unstable: strikes on Gulf energy assets continued for hours after the announcement, and Iran threatened to terminate the ceasefire, citing continued Israeli attacks against Iranian interests in Lebanon.

The Strait of Hormuz did not immediately reopen and Iran stated it would continue to control transits and levy a toll for safe passage. A return to pre-conflict shipping flows in the immediate term is very unlikely, and a return to pre-conflict flow rates in the short term is unlikely.

Affected countries have, where possible, drawn down reserves as a short term measure and are attempting to diversify their sources of energy, fertilisers, and chemical exports for the medium to long-term. Across APAC, governments have also enacted supply-side controls such as a temporary ban on exports and producer mandates, and advised or mandated demand-suppression measures such as shorter work-weeks, reduced operating hours, fuel rationing, planned rolling blackouts, etc. Fuel shortages, fuel price hikes, rising costs of living, and economic crises are notable motivators of protests and riots in many countries in the APAC region.

Dependence on hydrocarbons

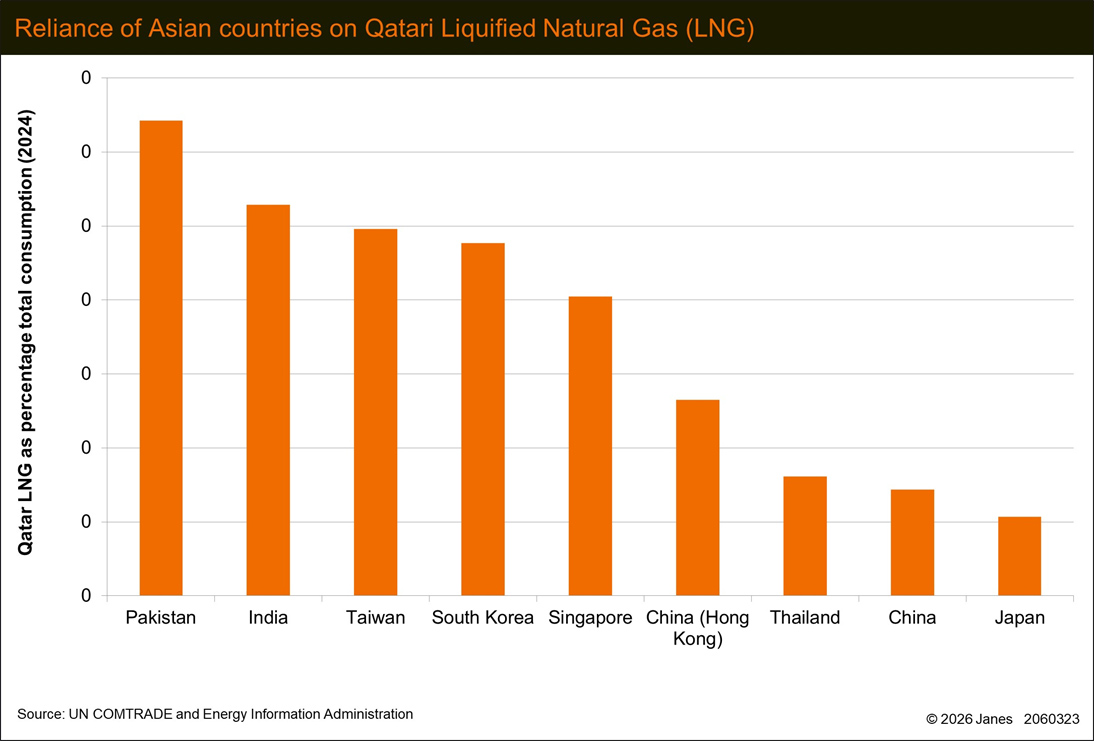

The impact on individual Asia-Pacific states – in terms of energy supply disruption and the political, institutional and economic capacity to offset the impact of disruption – is variable. Janes analysis indicates that Pakistan, India, Taiwan, and South Korea have the highest exposure to Qatari natural gas supplies in terms of the percentage of their own gas consumption met by Qatar (chart 1).

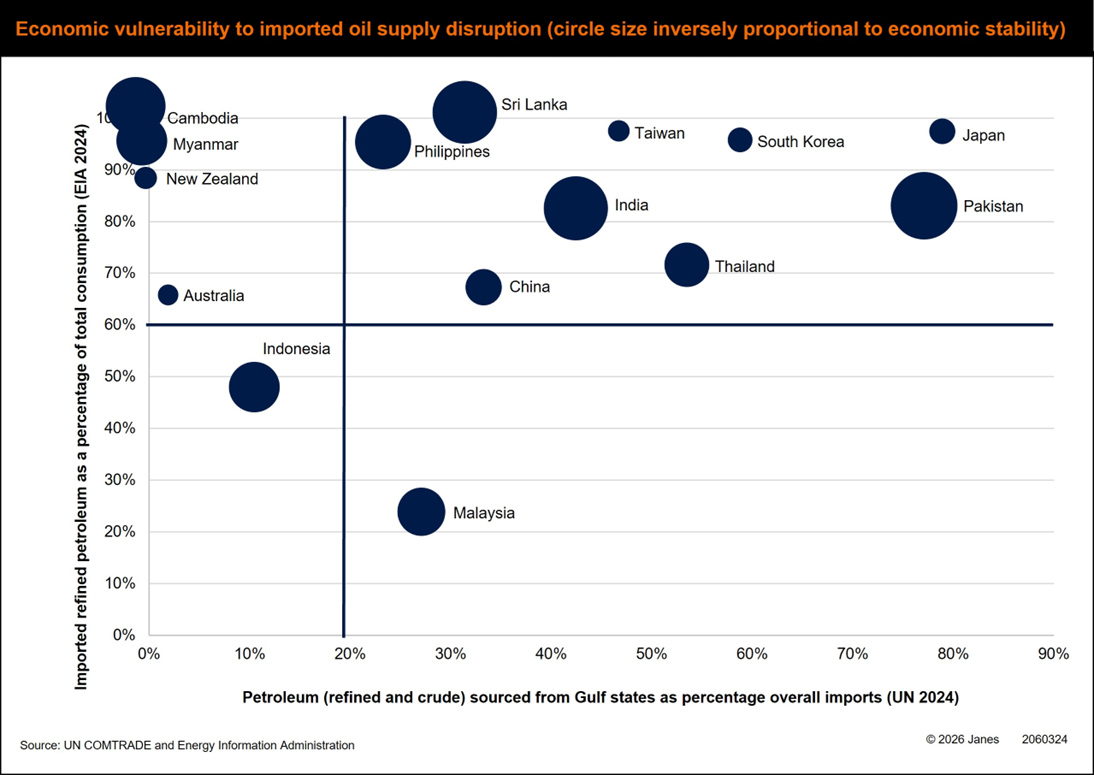

In terms of reliance on imported oil to meet domestic requirements – and the percentage of that oil that is sourced from the Gulf – Janes analysis indicates that Pakistan, India, Sri Lanka and Thailand are the most likely to be exposed when underlying economic stability (as expressed through the Janes Country Stability Indicators) is taken into consideration (chart 2).

Considering the overall economic and resource reliance picture of Asia-Pacific countries, Janes analysis – based on oil imports as a percentage of GDP, current account balance, foreign currency reserves, net energy dependence, and external debt – indicates that Sri Lanka, Pakistan, and the Philippines exhibit the highest vulnerabilities.

Vulnerability to Gulf linked energy disruption in the Asia Pacific is uneven but concentrated among a small group of states where high import exposure coincides with limited economic and institutional capacity to absorb shocks.

Exposure varies significantly across the region, reflecting differences in energy import profiles and in the political, institutional, and economic capacity to offset disruption. Janes analysis shows that Pakistan, India, Taiwan, and South Korea have the highest exposure to Qatari natural gas supplies, measured as the share of national gas consumption met by Qatar in 2024 (chart 1).

Oil related vulnerability is more acute where high import dependence on Gulf supply intersects with weaker underlying economic stability. On this basis, Pakistan, India, Sri Lanka, and Thailand emerge as the most exposed, when reliance on imported oil and the proportion sourced from the Gulf are assessed alongside underlying economic stability (as expressed through Janes Country Stability Indicators - chart 2).

India is, however, cushioned by the depth of its reserves and a diversified supplier base that could feasibly be leveraged to a greater degree. As per Indian government figures, India has 74 days' worth of reserve capacity ((including crude stocks, products stocks and dedicated strategic storage) and on 26 March, an additional two months' worth of crude had been procured. India imports oil and oil products from 41+ suppliers and Liquefied Petroleum Gas (LPG) supplies were being procured from countries such as Australia, Russia, and the United States, thereby reducing the impact on supply due to the crisis in Iran.

Taking a broader view of economic and resource dependence, Janes analysis—based on oil imports as a percentage of GDP, current account balance, foreign currency reserves, net energy dependence, and external debt—indicates that Sri Lanka, Pakistan, and the Philippines exhibit the highest overall vulnerability to sustained supply disruption.

Janes assesses that mitigation measures introduced in March - including the release of 400 million barrels from strategic reserves announced by the International Energy Agency on 19 March; the temporary lifting of US secondary sanctions on Russian oil already at sea for a 30-day period from 12 March 2026; a comparable US waiver for Iranian oil already at sea announced on 20 March 2026; and limited, case-by-case arrangements reportedly made between some Asian states and Iran to permit transit through the Strait of Hormuz – will have reduced the immediate severity of supply disruption.

Reliance of Asian countries on Qatari LNG (2024). Charts shows LNG imports from Qatar as a percentage of total gas consumption.

Reliance of Asian countries on Qatari LNG (2024). Charts shows LNG imports from Qatar as a percentage of total gas consumption.

Image credit: Janes

Economic vulnerability of Asian countries to imported oil supply disruption. Circle size is derived from Janes economic Country Stability Indicators and is inversely proportional to economic stability.

Image credit: Janes

Chemical and industrial production

Exposure to disruption of Gulf sourced chemical feed-stocks poses a material risk to a subset of Asia Pacific economies where the chemical sector is economically significant and reliance on Gulf inputs is high.

The economic significance of chemical industries varies across the Asia Pacific region. In India and South Korea, the sector accounted for 13% and 10% of exports by value respectively in 2023, according to World Bank data. Fully 50% of naphtha used by South Korea typically originates in the Gulf, according to the Chosun news service. Disruption to chemical supply chains will therefore have direct implications for industrial output, employment, and broader economic stability.

Gulf states are a critical supplier of chemical feed-stocks as a by product of oil and gas production, notably naphtha, which underpins the manufacture of plastics, fibres, and solvents. The Asia Pacific region accounted for 56% of Gulf naphtha exports in 2024, with Thailand, Pakistan, Japan, and South Korea the principal recipients, according to UN COMTRADE data. Asia Pacific buyers also accounted for 47% of Gulf sulphur exports in 2024. Sulphur is a foundational input for fertiliser production and metals processing.

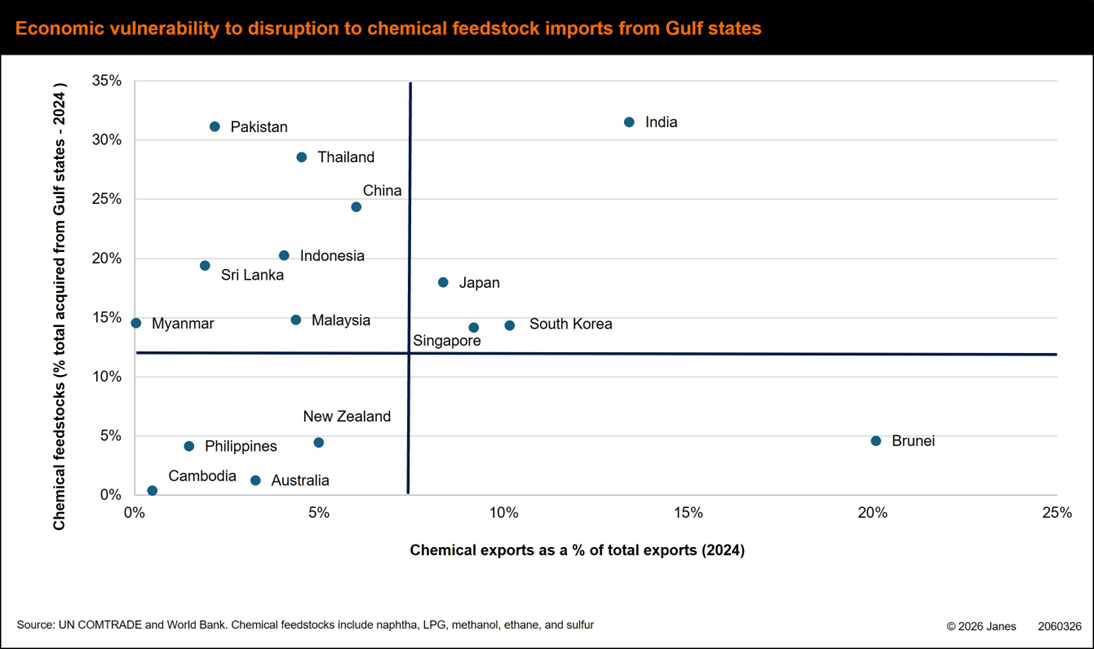

Assessing exposure based on the scale of chemical exports as a share of total national exports, indicating the economic importance of the sector, and reliance on Gulf-sourced feedstocks, Janes analysis indicates that India, Japan, and South Korea are particularly exposed to sustained disruption (chart 3).

For larger and arguably more resilient economies such as India, Japan, and South Korea, exposure is less likely to translate into acute instability, but disruption to chemical feedstocks and LNG supplies will still have economic effects, including reduced industrial output, supply chain dislocation, and likely knock on impacts on employment and export performance. These effects will be uneven across sectors and regions, increasing internal distributional pressures even where aggregate stability is maintained.

Economic vulnerability to disruption to chemical feedstock imports from Gulf states

Economic vulnerability to disruption to chemical feedstock imports from Gulf states

Image credit: Janes

For more, please see Iran Conflict 2026: Asia‑Pacific Faces Sustained Macro Shock from Gulf Supply Disruption