Assessing NATO's defence spending plans

Beyond the headlines: a reality check on NATO’s commitments

Guy Anderson and Andrew MacDonald - July 2025

“Together, allies have laid the foundations for a stronger, fairer, more lethal NATO,” said NATO Secretary General Mark Rutte at the close of the press conference that marked the conclusion of the alliance’s June 2025 summit in the Hague. “These decisions will have a profound impact on our ability to do what NATO was founded to do – deter and defend.”

The principal decision to which Rutte was referring was the agreement among ‘allies’ to commit to defence spending of at least 5% of GDP by 2035. This ambitious objective ostensibly signifies a significant step up for military budgets from the near 20 year ‘commitment to endeavour’ towards a spending threshold of 2% of GDP.

Beyond the greatly elevated spending target, which itself merits close attention, the event was notable for its narrow focus and a sharp acceleration of a recent trend towards greater brevity in the drafting of the summit declaration.

The declaration at the conclusion of the 2014 Wales summit – which included agreement to “aim to move towards the 2% [of GDP spending] guideline within a decade” ran to 13,000 words. The communique at the close of the 2024 Washington DC summit was reduced by more than half to 5,340 words, and the 2025 declaration was cut further to just 422 words.

Ironclad commitment to Article 5

The customary reaffirmation of the alliance’s ‘ironclad’ commitment to the Article 5 mutual defence clause was retained along with the note of gratitude to the host country. There was also the assertion of a ‘shared commitment’ to the removal of trans-Atlantic barriers to defence trade and industrial co-operation.

The remainder of the declaration, however, related to defence expenditure. Such narrow focus points towards a desire to avoid the derailment of core objectives and arguably to circumvent potentially damaging political disagreements that would have undermined displays of unit. The views and priorities of the United States President Donald Trump – who has been vocal in his demands that NATO members in Europe in particular make a greater contribution to the continent’s security – were also paramount.

Indeed, omissions from the declaration are notable. Russia was condemned as the “most significant and direct threat to allies’ security” in the 2024 declaration but had seemingly been downgraded to a “long-term threat” in the communique of 2025. Support for Ukraine was reaffirmed but the 2024 assertion that the country’s “future is in NATO” was not repeated.

Road to 5% defence spend

The core goal of spending 5% of GDP annually on “core defence requirements” and “defence and security related” needs by 2035 was divided into two tiered objectives. These were commitments to reach expenditure of 3.5% of GDP based on the ‘agreed definition of NATO defence expenditure’ – specifically funding to meet the needs of the armed forces – and a supplementary goal of 1.5% of GDP to ensure civil preparedness and resilience.

If the core objective of raising defence spending to 3.5% of GDP across the 32-member alliance were met, then NATO’s collective defence spending would reach USD2.4 trillion by 2035: a 63% real terms increase from the current leveli. This, of course, seems improbable given that by 2024 only half of NATO members had reached the prior 2% of GDP objectiveii.

Unlike the supplementary 1.5% of GDP objective (which provides substantial scope for interpretation), the core goal is both well-defined and subject to a firmer commitment than prior spending objectives. NATO defence ministers agreed in 2006 to a “commitment to endeavour” towards the goal, and in reaffirming the objective in 2014 merely aimed “to move towards the 2% guideline within a decade”. The 3.5% of GDP target, in contrast, was subject to a ‘commitment’ by ‘allies’.

Here too, however, there was room for interpretation: ‘allies commit’ arguably lacked the unanimity of the ‘we’ employed elsewhere in the declaration and permitted countries such as Spain (which publicly distanced itself from the target ahead of the summit) to endorse the final text.

The supplementary goal of 1.5% of GDP is intended to cover the “protection of infrastructure, defend our networks, ensure … civil preparedness and resilience, unleash innovation, and strengthen [NATO’s] defence industrial base” among other things. This ‘inter alia’ provision permits substantial interpretation on the part of member states, and it is easy to see how more general infrastructure investment could be added to this ledger. Italy, for example, is reportedly looking to include civilian infrastructure including ports and even a previously announced bridge linking Sicily to the mainland under defence and security investmentiii.

Support for Ukraine too – in the form of “direct” contributions towards its defence and support for its defence industrial base – is permissible against the supplementary goal. Support for the Ukrainian armed forces from European Union (EU) member states alone (85% of whom are NATO members) had reached EUR53.5 billion (USD62.4 billion) by mid-2025, according to European Council figuresiv.

Meeting NATO’s defence spending goal

Adherence to prior NATO spending goals was far from universal. Janes Defence Budgets data shows that just 19% of alliance members met the 2% of GDP spending threshold in 2021, although the changed security environment in Europe resulting from Russia’s full-scale invasion of Ukraine in 2022 shifted the overall emphasis on military investment. By 2025 more than half of members reached the 2% goal. Janes forecasts that about 63% of the members will commit to the 2% goal by 2028.

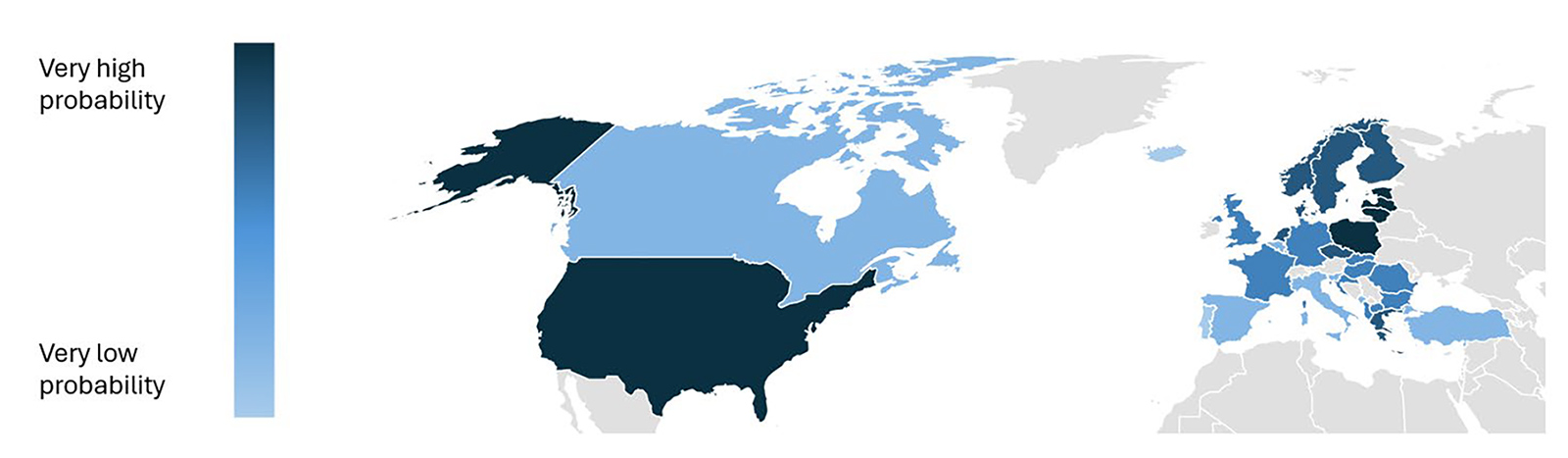

Factors driving defence spending are myriad, and Janes took these into account to model the probability of NATO member states reaching an enhanced goal of 3% of GDP by 2030 (a level and timeframe considered plausible in the months prior to the June 2025 NATO summit).

Specifically, Janes considered:

The existing level of national defence expenditure (including how close this is to the higher objective)

The status of defence spending in the domestic political landscape (for example, if a defence spending floor is enshrined in law or subject to broad political consensus)

Threat factors (combining the overall external security environment based on Janes Country Stability Indicators external stability rating with the geographical distance between Moscow and the member state’s capital city)

Sensitivity to past inflexion points (including Russia’s occupation of Crimea and the global financial crisis)

Political and social factors (according to the qualitative analysis of Janes analysts).

Janes concluded that 69% of NATO members are likely to reach 3% of GDP by 2030 (see figure 1), and that 38% of members would likely meet an even higher goal of 5% of GDP.

Probability of NATO member states meeting an elevated defence spending target of 3% of GDP (core expenditure) by 2030. Source: Janes. 2060295

Probability of NATO member states meeting an elevated defence spending target of 3% of GDP (core expenditure) by 2030. Source: Janes. 2060295

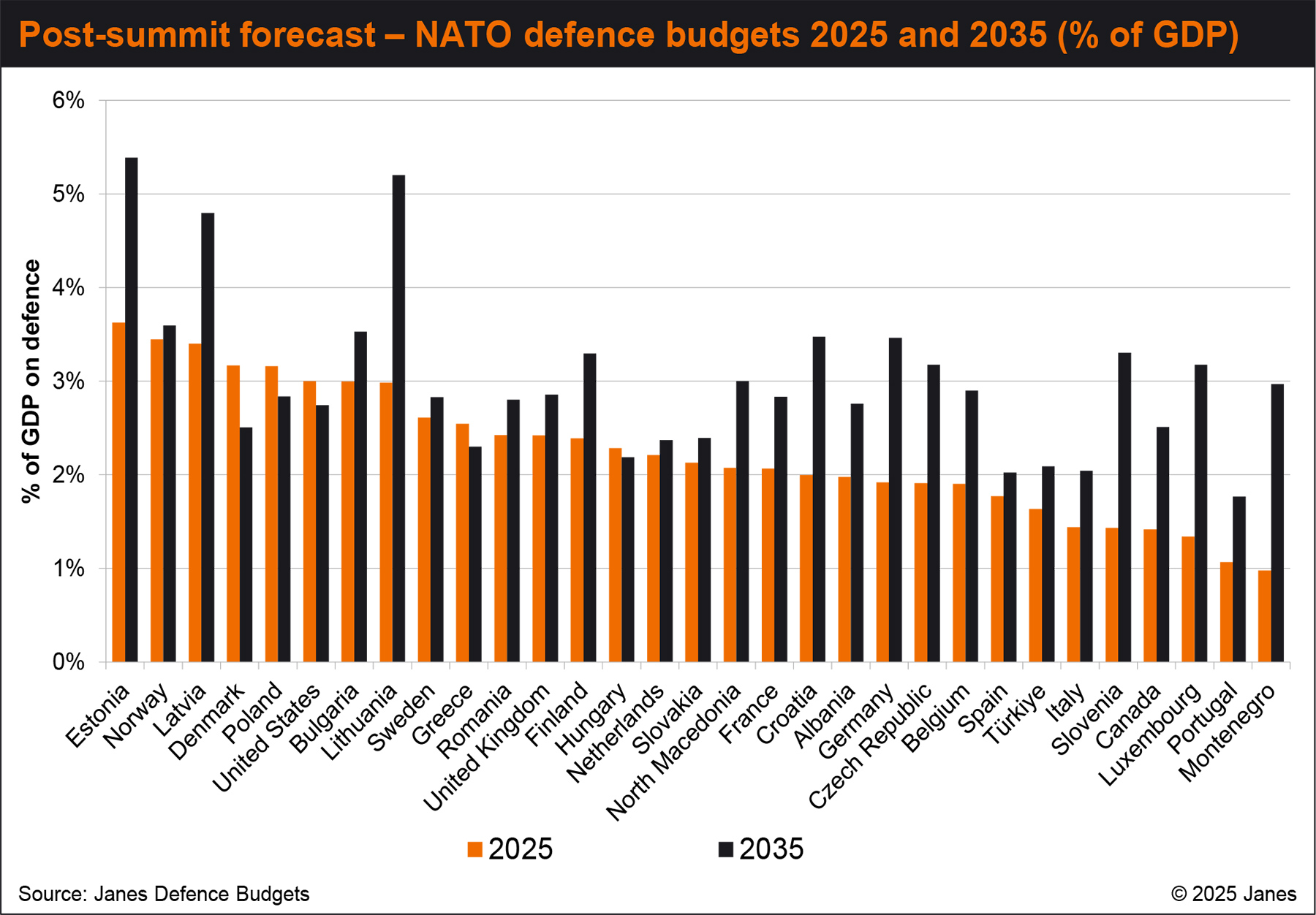

Findings from this modelled approach are reinforced by Janes analyst-led defence budget forecasts, which were updated frequently in the first half of 2025 to reflect the publishing of new official targets as well as in the aftermath of the NATO summit. Several countries proceeded with major changes to their funding plans in preparation for the alliance’s commitment, announcing their own goals in anticipation of the increased commitment (see figure 2).

The German government’s release of its 2025 budget the day before the summit , for example, including projections of reaching 3% of GDP by 2029, appeared to be particularly timely fiscal theatre, but it joined several important alliance members who had already published plans to greatly increase their spending in relation to the size of their economies; albeit with varying degrees of commitment and plausibility.

The UK’s government has pledged to reach 3% of GDP by 2032 and France’s President Emmanuel Macron revealed an aspiration of 3–3.5% by 2030, although domestic politics are likely to hamper efforts in both cases.

Poland’s defence budget exceeded the new target even in 2024, when it was worth 3.6% of GDP, even before inclusion of a dedicated modernisation fund (which is financed by borrowing repaid by future Ministry of National Defence budgets and therefore excluded from Janes Defence Budgets totals)

The Netherlands had already committed to a 3.5% target, but had no timeframe to achieve it, while all of the Nordic countries – Iceland aside – either had pre-summit plans to meet the 3.5% target, or had already come fairly close, with Norway and Denmark examples of the latter.

Of the NATO budgets currently above USD10 billion, Italy, Spain, Türkiye, Canada, and (given

the minority government’s loose grip on the legislative process) France look uncertain in their ability to reach the new 3.5% target within a decade – though the UK’s plans also look vulnerable to an austere fiscal environment.

Even if alignment with the 3.5% target is variable and incomplete across the alliance, partial implementation is expected to produce a major impact. On a country-by-country basis, by 2035 average NATO spending as a percentage of GDP is expected to have grown from 2.2% to 3.0%.

Post-summit forecast: NATO defence budgets, 2025 and 2035. Source: Janes Defence Budgets. 2060296

Post-summit forecast: NATO defence budgets, 2025 and 2035. Source: Janes Defence Budgets. 2060296

Headwinds against defence spending growth

The requirement to find additional funding for defence and security investment comes at a challenging time for NATO member states given the enduring fiscal impact of the Covid-19 pandemic, the subsequent inflationary shocks associated with the recommencement of global trade and Russia’s full-scale invasion of Ukraine, and the already weak economic trajectory of many alliance members.

State debt and budget deficits have – in many cases – become elevated as a result of the demands of the pandemic. In 2019 the average deficit of a NATO member state was half of 1% of GDP compared with 2.3% by 2025. Borrowing costs have also become elevated since the Covid-19 crisis. As an example, Germany – the benchmark for European borrowing costs – was able to borrow at a rate of less than 1% prior to 2020 compared to closer to 3% today.

The EU attempted to address spending requirements through the ReArm Europe Plan/Readiness 2030 programme: a package of measures permitting member states to deviate from deficit and borrowing limits and to access European Commission-backed credit to fund greater defence spending. While the package would ease the path to 3.5% of GDP for NATO and the EU’s common members, it is not cost-free and challenges – ranging from competing spending priorities to the sustainment of deficits in a challenging fiscal climate – will remain.

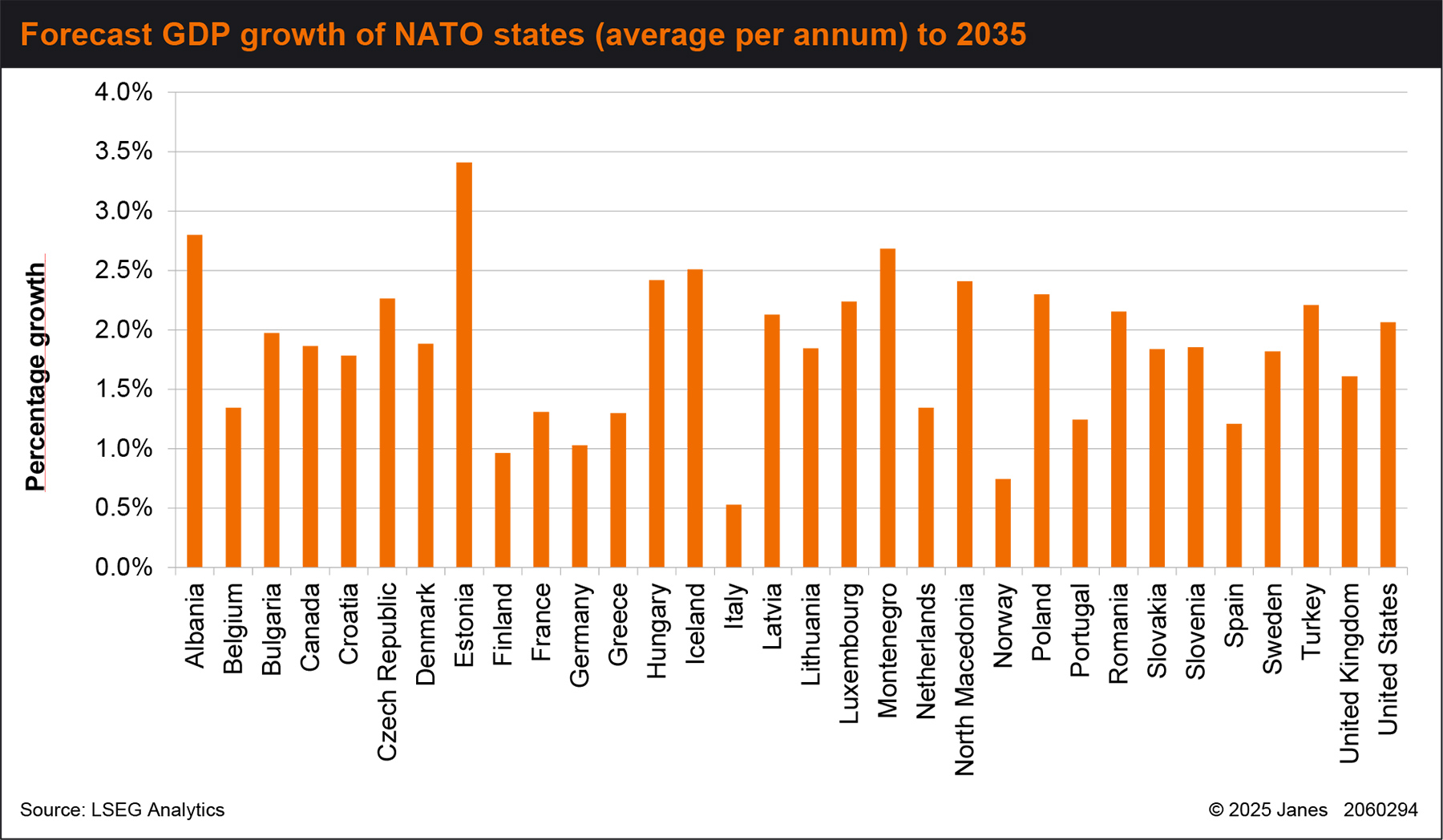

Of greater concern, however, must be the subdued economic environment. Forecasts from financial market data provider LSEG Analytics indicate that growth among NATO members will average less than 2% per annum over the next decade (see figure 3). In the absence of growth there is inevitably a zero-sum element to government spending decisions that indicates politically challenging choices will have to be made.

Other domestic spending priorities will likely place increasing demands on limited state budgets, even if some of these are assigned to the new 1.5% of GDP category. Social benefits and pensions, funding for healthcare, education, and other services will continue to be given higher priority by most European populations, and the pressure on governments to improve the living standards of their populations will increase as historically dominant parties are challenged by competitors from the political fringes.

Forecast GDP growth of NATO member states (average per annum) between 2025 and 2035. Source: LSEG Analytics. 2025 Janes: 2060294

Success?

The 2025 Hague summit can be viewed as a political success of sorts. Unity was broadly maintained, a unanimous reassertion of Article 5 (and therefore to the alliance itself) was made, and a broad pledge to increase defence spending was reached. Critically, the US appeared pacified by the commitments of its fellow alliance members. That defence spending across NATO has been – and will very likely remain – on a positive trajectory is not in doubt, although universal compliance with summit’s core spending objective of at least 3.5% of GDP seems far less likely.

The supplementary goal – addition up to 1.5% to core funding – is open to a tremendous amount of interpretation, indeed perhaps knowingly so. Spending under this account will be reviewed, but not until 2029.

Compliance aside, the political leaders who subscribed to the summit declaration have now returned to their capitals to face the challenge of making good on their commitments against headwinds of adverse fiscal conditions, competing spending demands, and subdued economic growth. The road to 2035 will pass through numerous elections with no guarantee that commitments made in 2025 will survive the ballot box. The security challenges facing Europe, meanwhile, remain unenviable.