Rearming Europe? Funding the rebirth of European defence

Date Posted: 12th May 2025

Updated: 19th May 2025

Author: Guy Anderson and Andrew MacDonald

“We are living in the most momentous and dangerous of times,” began a press statement issued by European Commission president Ursula von der Leyen on 4 March 2025. “I do not need to describe the grave nature of the threats that we face. Or the devastating consequences that we will have to endure if those threats come to pass.”

The substance of Von der Leyen’s announcement was scarcely less dramatic. The European Union (EU) would use its gold-plated credit rating to borrow EUR150 billion (USD170 billion) to fund European defence investment and again activate the national escape clause of the Stability and Growth Pact to allow member states to breach deficit and debt limits to fund rearmament.

The commission hoped that the European Readiness 2030 (formerly ReArm Europe) plan would ultimately increase defence spending by EUR800 billion by 2030, although this figure appears aspirational.

The road to 2025 - rebuilding European military capability

The factors leading to the commission’s announcement have been well documented. Europe is facing its starkest security environment for decades against a backdrop of competing security priorities of the United States, its strongest ally. The plan is intended to reverse a prolonged period of under-investment in defence and to rebuild military capability.

The trail of initiatives leading up to the European Readiness 2030 announcement can, however, be traced back almost a decade and were characterised by more tentative efforts to address capability gaps, hitherto limited co-operation between EU member states, technological shortcomings, and industrial capacity.

The European Defence Fund (EDF) and the associated Permanent Structured Cooperation (PESCO) were launched in 2017 to support intra-community defence and security research and development projects, although crucially the EU stopped short of centrally funding military procurement. EUR7.3 billion was committed to the fund between 2021 and 2017.

Activation of PESCO and the formation of the EDF owe much to a range of factors that focused European minds on the security environment, including Russia’s annexation of Crimea in 2014, the United Kingdom’s decision to leave the EU in 2016, and the commencement of the first administration of Donald Trump as US president in 2017.

Russia’s full-scale invasion of Ukraine in early 2022 prompted further measures by the EU, this time targeting industrial capacity (supply) and member state capability gaps (demand). Both the Regulation on Supporting Ammunition Production (ASAP) and the Regulation Establishing an Instrument for the Reinforcement of Industry through Common Procurement (EDIRPA) were announced in 2022 and adopted in 2023. The former committed EUR500 million to projects to increase ammunition production while the latter provided EUR300 million for multilateral ammunition, air and missile defence, and legacy platform replacement programmes.

Collectively, the pre-2025 projects were transformational in symbolism only. They marked a strong statement of intent and EDIRPA in particular stood out as the first time the commission had provided central funding for defence equipment. The funds committed, however, were insufficient to drive real capability change.

European Readiness 2030

At the core of the European Readiness 2030 plan are five pillars: the core Security Action for Europe (SAFE) financial mechanism (through which up to EUR150 billion will be raised), the activation of the Stability and Growth Pact escape clause to allow greater debt and deeper deficits among member states, the diversion of cohesion funds towards strengthening defence and security capabilities, and the mobilisation of private capital into defence (pillars four and five).

Pillars one and two have arguably generated the most debate given the scale of spending proposed. Funding of EUR150 billion would be equivalent to around 12% of combined EU member state defence spending between 2020 and 2024 [note: based on JDB data]. The EC’s proposal to effectively ring-fence funding to the industries of the EU, the European Free Trade Area and European Economic Area, Ukraine and potentially accession states and countries with which the EU has a Security and Defence Partnership (for example Japan and South Korea) also means that funding will be primarily concentrated in the bloc, and thus building on the ‘Fortress Europe’ aspect of previous policies including the European Defence Fund. The United States – a major supplier of European defence systems – will be excluded, although the UK’s entry into a Security and Defence Partnership with the EU in May 2025 potentially opened the door to participation.

The challenge for the EU and its member states, however, is that in some respects, the defence package could scarcely have been announced at a worse time.

Challenges ahead for increased defence spending?

The Covid-19 pandemic shrunk the economies of the EU, which combined with mitigation measures, pushed up debts and deepened deficits. The bloc’s fiscal rules were suspended for the first time in more than 20 years and then remained suspended as Russia’s full-scale invasion of Ukraine drove up energy prices and disrupted economic activity. Revised fiscal rules were reapplied from April 2024, less than a year before the current proposal to suspend them once again. By 2023 the overall deficit of the EU’s 27 member states stood at 3.5% of GDP and their total debt at EUR14.15 trillion. Growth was anaemic even prior to the succession of crises and the outlook remains weak.

The economies of the bloc are therefore ill-placed overall to take on more debt although levels of government debt vary greatly.

The EU as an institution has also increased its borrowings because of the pandemic through the Recovery and Resilience Facility (RRF), with EUR312 billion provided to member states as grants and a further EUR360 billion as loans. The debt falls due for repayment from 2028 and threatens to eat up to 10% of the EU’s annual budget unless some or all of it can be rolled over.

The RRF bonds were financed at costs at or close to zero, although the shifted interest rate environment means European Readiness 2030 costs will be significantly higher (likely around 3%). Whether member states choose to access central EU funding will depend greatly on their own borrowing costs, and paradoxically the southern EU countries with the least incentive to invest in defence (given their distance from Russia) would in general be prime candidates for the SAFE mechanism.

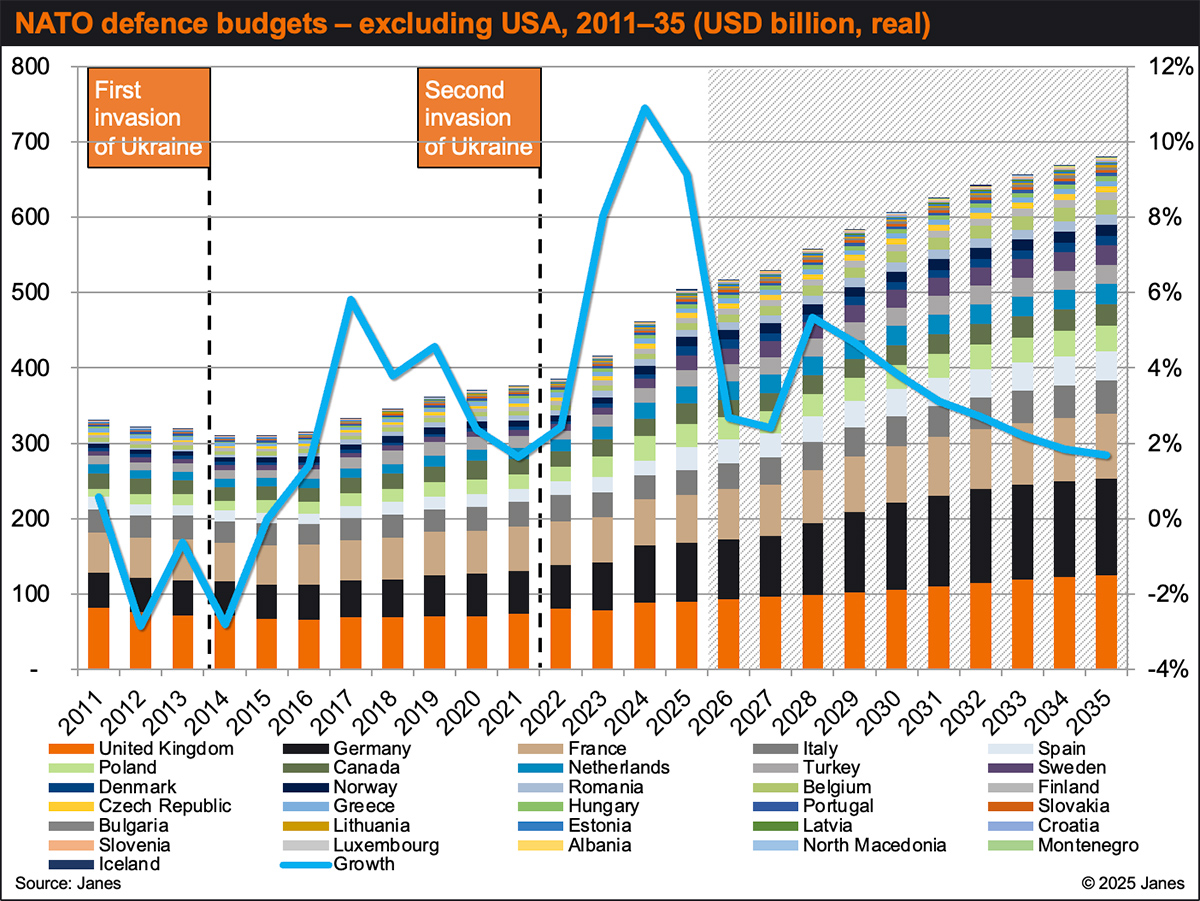

Defence spending in Europe

A fundamental question is why it took three years of warfare on the fringe of Europe and the straining of diplomatic ties with the US to get to a point where one of the richest regions in the world began to consider measures to rekindle its own defence capabilities.

Part of the answer is that the realities of the present day were unthinkable in recent memory, and that Europe relied excessively on the US as a security guarantor of last resort.

In the decade to 2015 (encompassing the global financial crisis and the related eurozone crisis) defence spending in Europe was almost completely static in real terms. Russia’s annexation of Crimea – and arguably tangential factors like the UK’s decision to exit the EU and pressure to increase investment during the first Trump presidency – acted as an inflexion point, and spending in the bloc climbed 21% in real terms between 2015 and 2021.

It was also Russian aggression that prompted NATO’s 2014 Cardiff Declaration through which the alliance’s 2% of GDP spending target shifted from guidance to a commitment.

NATO military spending threshold and growth

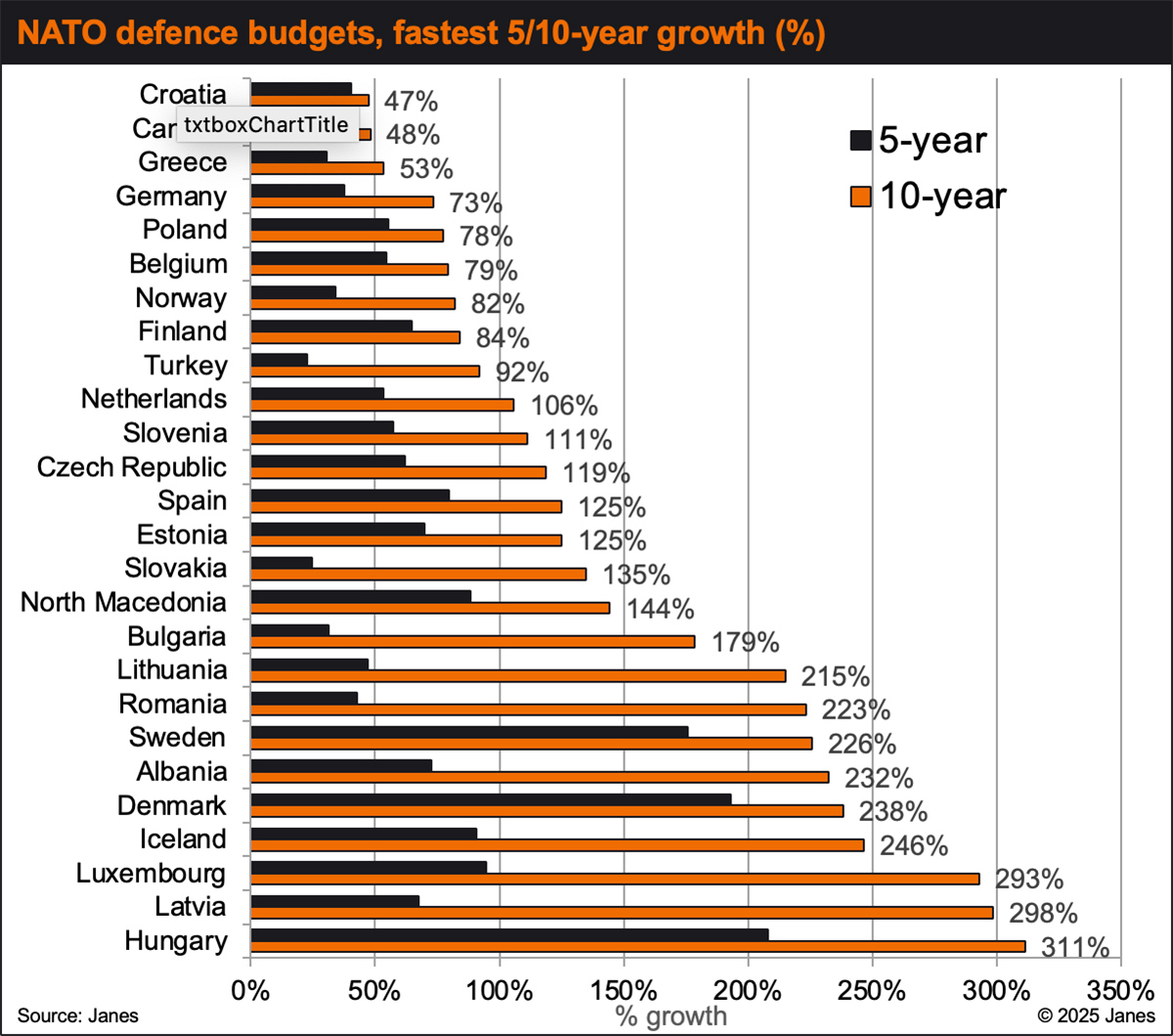

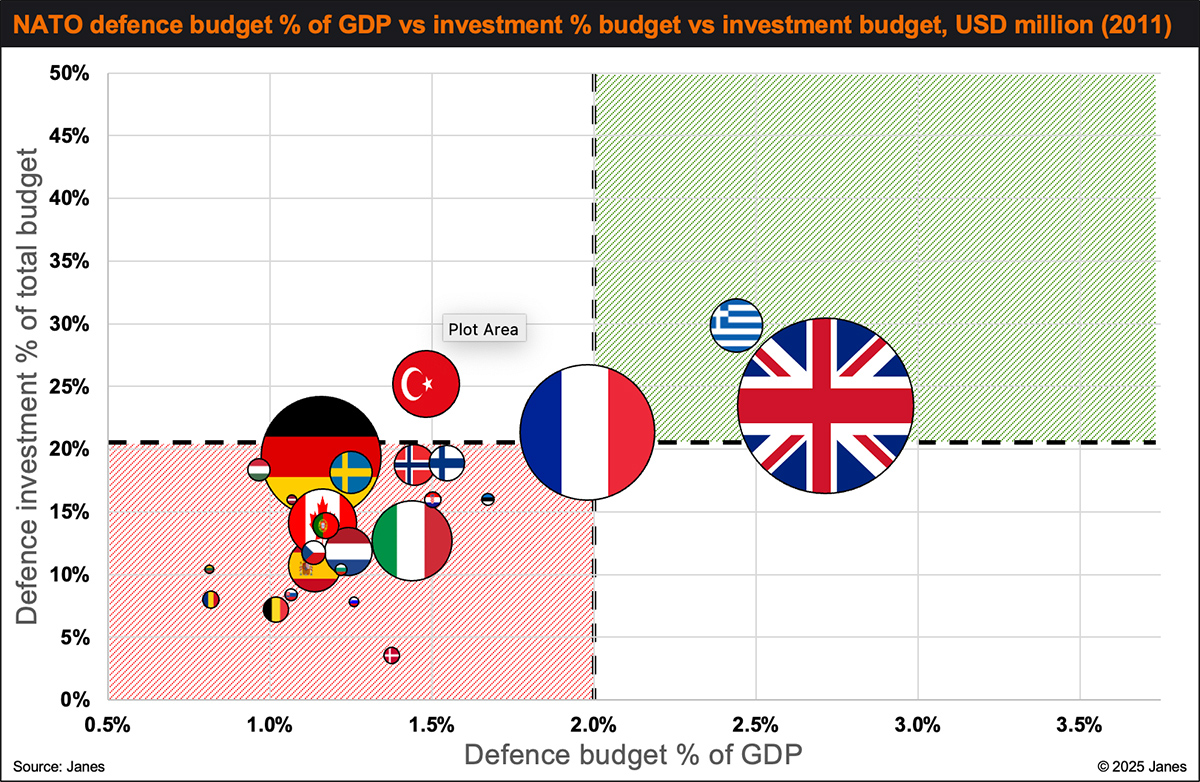

Prior to the agreement of the 2% of GDP spending threshold, only France, the UK, and (intermittently) Greece fulfilled both overall and investment targets. By 2021 Eastern Europe had made notable progress, although it took Russia’s full-scale invasion of Ukraine to drive deep change to Europe’s defence spending.

At present, 17 non-US NATO members meet the 2% goal and virtually all meet the associated target of dedicating 20% of defence spending to investment. Janes forecasts that by the early 2030s 19 countries will fully have reached both the spending benchmarks with an average non-US NATO defence budget of 2.3% of GDP.

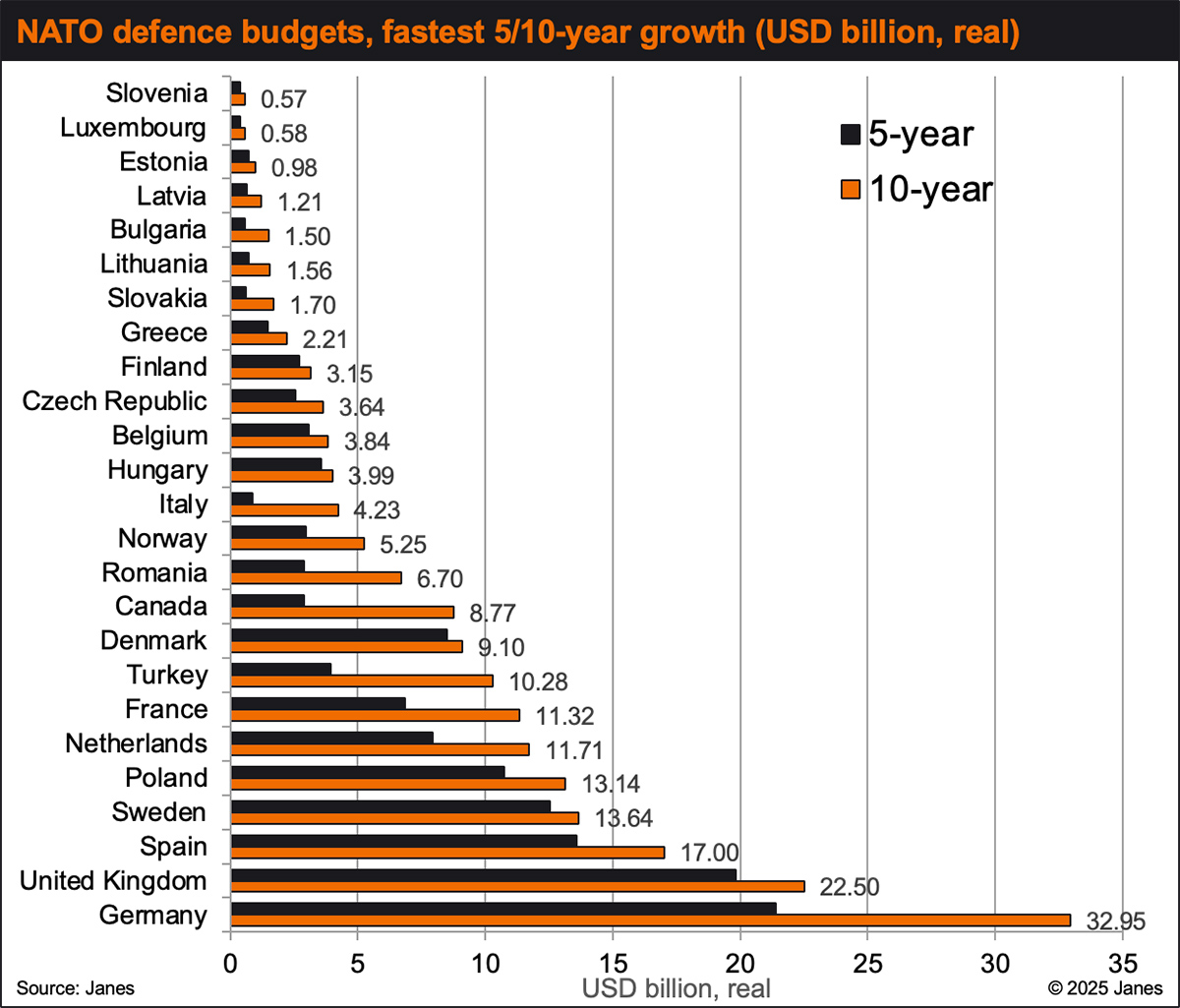

Of note has been the scale of European defence spending growth among both NATO and non-NATO member states since 2022. Of the 33 European defence markets tracked by Janes Defence Budgets, 16 have implemented their fastest ever rate of growth in the years since 2022. These include France, Germany, Poland, Spain, Ukraine, and the United Kingdom, which have all broken expansion records.

Outlook for the European Readiness 2030 initiative

The generational threat facing Europe and the change in the security priorities of its strongest ally, the US, has focused the minds of policy makers. That European defence spending is on a growth trajectory is beyond question, and the European Readiness 2030 plan and related measures have the potential to clear obstacles to the rebuilding and augmentation of capabilities.

From financial, social, and political perspectives, however, defence investment is not cost-free. European economic growth has been anaemic and will likely remain so over the coming years which will put national budgets (and debt sustainability in some cases) under pressure.

Difficult trade-offs will need to be made and pressure on non-defence budgets (potentially social spending in some cases) may lead to political shifts.

Given that higher spending is not an objective in itself, the result of these initiatives must be in question. The objectives of the earlier ASAP and EDIRPA programmes were clear with the former focused on ammunition capacity (explosives, powder, shells, missiles, and related testing and certification) and the latter on support for the procurement of ammunition, air and missile defence systems, and platforms and legacy vehicle replacement. The procurement priorities under European Readiness 2030 will inevitably go further, and clarity will be essential to ensure the coherent development of European capability overall.

The ring-fencing of funding under SAFE to Europe and specific allies will help bolster defence industrial investment confidence, although here too, clarity on specific requirements over an adequate timescale will also be required.

Finally, there is the perennial question of European cooperation to reduce duplication of effort while also avoiding the sort of unwieldly multinational participation that makes greater political than economic or strategic sense.

To return to von der Lyon’s market moving press statement, Europe is in an “era of rearmament” and must take on “much more responsibility for [its] own European security”.

“This is Europe’s moment, and [it] must live up to it.”

For further discussion listen to our latest podcast here: Rearming Europe? Funding the rebirth of European defence

Appendix